Recommended Blog Posts

- Housing Costs in Canada for Newcomers (2026): Rent, Deposits, Utilities & Smart Saving Strategies

- Banking and Credit System in Canada for Newcomers: Accounts, Credit Score, Money Transfers and Daily Expenses

- Taxes & Government Benefits in Canada for Newcomers: Maximize GST Credits, Child Benefits, and Tax Refunds

- Transportation & Daily Mobility In Canada: Which Insurance Would Be Best for Newcomers?

- Education & Childcare in Canada: Costs, System, and What Newcomers Must Know in 2026

How to Apply for Your Canadian Health Card: A First-Week Checklist

Publish On: July 01, 2026

Healthcare is one of the most important things newcomers must understand before arriving in Canada. Canada has a publicly funded healthcare system, but coverage is managed by provinces and territories, which means the rules are not exactly the same across the country.

Permanent residents, work permit holders, and international students may have different eligibility rules depending on where they live. Some newcomers may get provincial health coverage quickly, while others may need private health insurance during a waiting period.

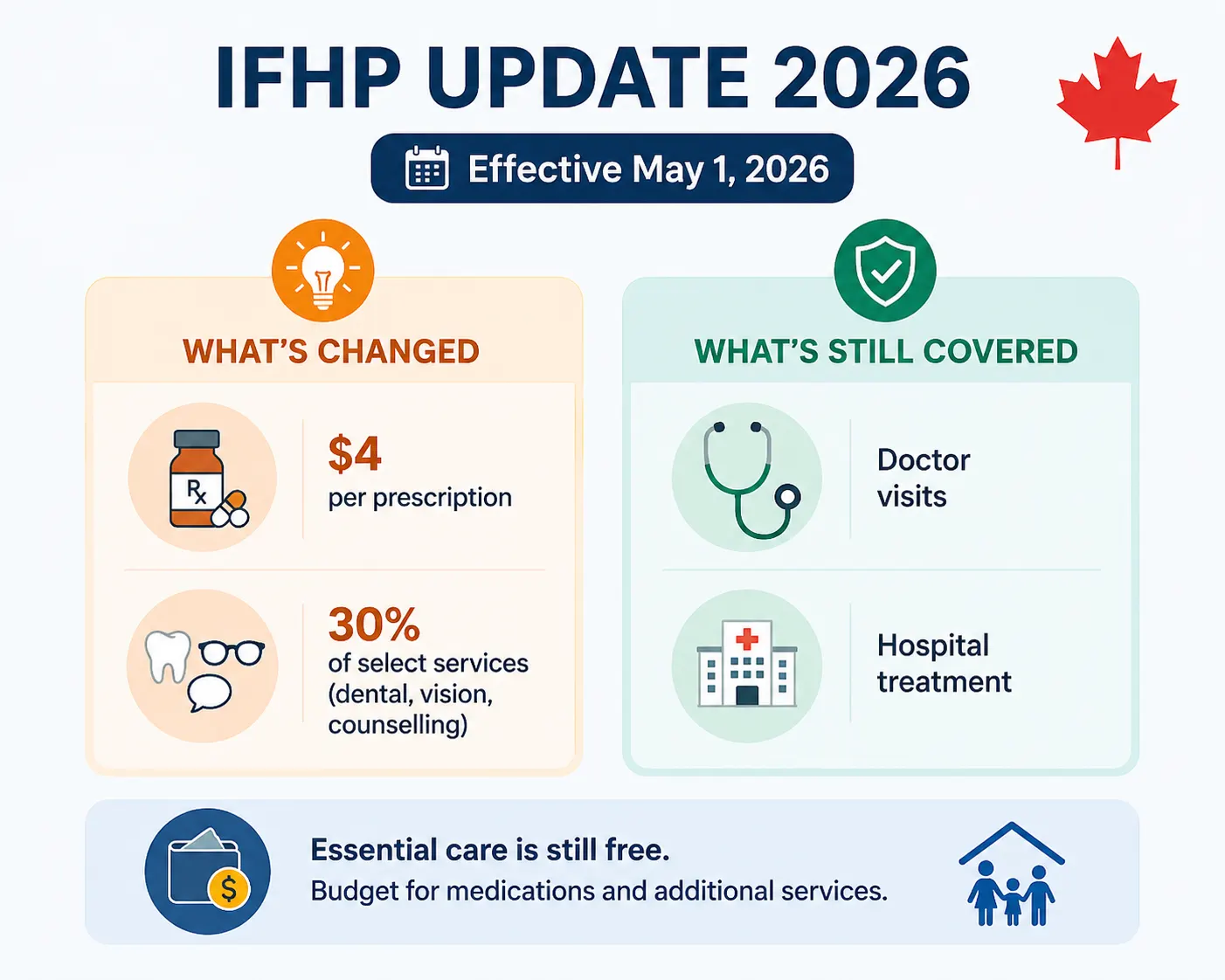

IFHP Update 2026: Starting May 1, 2026

Canada has made a small but important change to the Interim Federal Health Program (IFHP), starting May 1, 2026. Until now, IFHP covered most healthcare costs for eligible newcomers. With the new update, it’s no longer fully free for everything.

What’s Changed

- You’ll pay $4 per prescription

- You’ll cover 30% of certain extra services like dental, vision, and counselling

What’s Still Covered

- Doctor visits

- Hospital treatment

These essential services remain completely free.

Why Healthcare Planning Matters for Newcomers

Many newcomers assume that healthcare becomes free immediately after landing in Canada. In reality, provincial coverage may not begin right away, and some services are not fully covered even after you receive your health card.

This matters because medical care without insurance can be expensive. A doctor visit, emergency room visit, ambulance ride, prescription medication, dental procedure, or eye exam may create unexpected financial pressure if you are not prepared.

| Healthcare Area | Why It Matters |

|---|---|

| Provincial Health Coverage | Determines whether doctor visits and hospital care are covered. |

| Waiting Period | Some newcomers may need temporary private insurance before coverage starts. |

| Private Insurance | Helps cover medical costs during gaps or for services not covered publicly. |

| Prescription Drugs | Medication may not be fully covered by provincial health plans. |

| Dental and Vision Care | Usually not fully covered under basic public healthcare. |

| Emergency Costs | Without insurance, emergency treatment can become very expensive. |

How Canada’s Healthcare System Works

Canada’s healthcare system is publicly funded, but each province and territory runs its own health insurance plan. This means your eligibility, documents, waiting period, and coverage start date depend on where you live.

Once approved, provincial health insurance usually covers medically necessary hospital and physician services. However, it does not automatically cover every healthcare expense.

| Coverage Type | Usually Covered by Provincial Health Plans? | Important Note |

|---|---|---|

| Doctor Visits | Yes | Covered when medically necessary and after eligibility starts. |

| Hospital Care | Yes | Covered for insured residents under provincial plans. |

| Emergency Care | Yes, once insured | Uninsured newcomers may need to pay full costs. |

| Prescription Drugs | Limited or varies | Often requires private, employer, student, or provincial drug coverage. |

| Dental Care | Usually no | Routine dental services are often paid privately. |

| Vision Care | Limited or varies | Eye exams, glasses, and contact lenses may not be fully covered. |

Provincial Health Coverage Eligibility for Newcomers

Provincial health coverage eligibility depends on your immigration status, province of residence, and whether you meet local residency rules. Permanent residents are generally eligible, but work permit holders and international students may face additional conditions.

Newcomers should apply for their health card as soon as they arrive and have the required documents. Delaying the application can delay access to insured healthcare services.

| Newcomer Type | Typical Eligibility Situation | Important Planning Tip |

|---|---|---|

| Permanent Residents | Generally eligible for provincial health coverage. | Apply immediately after arrival or once residency requirements are met. |

| Work Permit Holders | May be eligible depending on permit type, duration, and province. | Check province-specific eligibility before arrival. |

| International Students | Eligibility varies significantly by province. | Confirm whether public, private, or school insurance applies. |

| Visitors | Usually not eligible for provincial health coverage. | Private travel medical insurance is strongly recommended. |

Health Coverage Waiting Periods by Province

Some provinces provide coverage immediately after eligibility is confirmed, while others may apply a waiting period. During this period, newcomers may need private health insurance to avoid paying medical costs out of pocket.

Waiting periods and eligibility rules can change, so newcomers should always confirm the latest requirements from the official provincial health ministry before moving.

| Province | Health Plan | Waiting Period / Eligibility Note |

|---|---|---|

| Ontario | OHIP | No general three-month waiting period currently, but eligibility documents are required. |

| British Columbia | MSP | Coverage may begin after the balance of the arrival month plus two more months. |

| Nova Scotia | MSI | Eligibility and timing depend on residency and status; newcomers should verify before arrival. |

| Manitoba | Manitoba Health | Eligibility depends on immigration status and residence; some temporary residents may not qualify immediately. |

| Alberta | AHCIP | Coverage may start when residency requirements are met; rules depend on move type and status. |

| Quebec | RAMQ | A waiting period may apply for some newcomers. |

The safest approach is to arrange private insurance for your first months in Canada unless you have confirmed in writing that your provincial coverage starts immediately.

Private Health Insurance for Newcomers

Private health insurance is a short-term safety net for newcomers who are not yet covered by provincial healthcare. It is especially important during waiting periods, temporary stays, or the early settlement phase.

A private plan can help cover emergency medical treatment, doctor visits, hospital stays, diagnostic services, ambulance costs, and certain medications depending on the policy.

| Private Insurance Feature | Why It Helps Newcomers |

|---|---|

| Emergency Medical Coverage | Protects against high hospital and emergency treatment costs. |

| Doctor Visit Coverage | Useful before provincial health coverage begins. |

| Prescription Support | May cover eligible medication expenses based on the plan. |

| Ambulance Coverage | Helps reduce emergency transportation costs. |

| Temporary Protection | Useful for the first few weeks or months after arrival. |

Health Insurance for International Students in Canada

International students must pay special attention to healthcare rules because coverage depends heavily on the province and school. Some provinces allow eligible international students to apply for public health insurance, while others require private health insurance.

Many colleges and universities include mandatory health insurance plans in student fees. However, students should still check what the plan covers, whether dental and vision are included, and whether coverage starts from the arrival date.

| Student Healthcare Area | What Students Should Check |

|---|---|

| Provincial Coverage | Whether international students are eligible in that province. |

| School Insurance Plan | Whether the college or university provides mandatory coverage. |

| Coverage Start Date | Whether insurance begins on arrival or after classes start. |

| Dental and Vision Benefits | Whether the plan includes checkups, glasses, or dental care. |

| Prescription Drugs | Whether medications are partly or fully covered. |

Prescription Drug Coverage in Canada

Prescription drug coverage is one of the most misunderstood parts of Canadian healthcare. Even after receiving a provincial health card, newcomers may still need to pay for many medications unless they have additional coverage.

Drug coverage can come from employer benefits, private insurance, student insurance, provincial drug programs, or out-of-pocket payment. Eligibility and reimbursement depend on the province and plan.

| Drug Coverage Source | Who It May Help | Important Note |

|---|---|---|

| Employer Benefits | Full-time workers with benefit plans | Often covers a percentage of eligible prescriptions. |

| Private Insurance | Newcomers during waiting periods or without employer benefits | Coverage depends on the policy. |

| Student Insurance | International students | May include partial prescription coverage. |

| Provincial Drug Programs | Eligible residents based on province, age, income, or medical need | Rules vary across Canada. |

| Out-of-Pocket Payment | Anyone without drug coverage | Costs can add up quickly for long-term medication. |

Dental and Vision Care in Canada

Dental and vision care are not fully covered by most basic provincial healthcare plans. This means newcomers should budget separately for dental cleanings, fillings, eye exams, glasses, contact lenses, and related services.

Employer benefits, student plans, private insurance, or government dental programs may reduce costs, but coverage is not automatic for every newcomer.

| Service | Common Coverage Situation | Newcomer Planning Tip |

|---|---|---|

| Dental Cleaning | Usually private or benefit-based | Ask about student or employer dental plans. |

| Fillings and Dental Treatment | Usually not fully covered publicly | Costs can be high without insurance. |

| Eye Exams | Coverage varies by age, province, and medical need | Confirm provincial and private plan rules. |

| Glasses and Contact Lenses | Usually paid privately or through benefits | Compare costs before purchasing. |

| Orthodontics | Usually private | Often expensive and not included in basic coverage. |

Emergency Medical Costs Without Insurance

Emergency medical care without insurance can be financially risky. If you are not yet covered by a provincial health plan and you do not have private insurance, you may be responsible for the full cost of care.

Costs can include hospital fees, emergency physician charges, diagnostic tests, ambulance services, procedures, and follow-up treatment. This is why private insurance is strongly recommended before your coverage begins.

| Emergency Cost Type | Why It Can Be Expensive |

|---|---|

| Emergency Room Visit | Hospitals may bill uninsured patients directly. |

| Ambulance Service | Ambulance fees may not be fully covered even for insured residents in some cases. |

| Hospital Admission | Daily hospital charges can be significant without insurance. |

| Diagnostic Tests | Blood tests, imaging, and scans may be billed if uninsured. |

| Surgery or Specialist Care | Uninsured procedures can create major financial liability. |

Healthcare Checklist for Newcomers

A simple healthcare checklist can help newcomers avoid gaps in coverage. The goal is to know your province’s rules before arrival and protect yourself during the first few months.

This checklist is useful for permanent residents, international students, work permit holders, and families moving to Canada.

- Check your province’s health coverage eligibility before arrival.

- Confirm whether a waiting period applies.

- Buy private health insurance if coverage does not start immediately.

- Apply for your provincial health card as soon as you are eligible.

- Keep copies of immigration documents, proof of address, and identity documents.

- Check whether your school or employer provides health benefits.

- Budget separately for prescription drugs, dental care, and vision care.

- Keep emergency insurance active until provincial coverage is confirmed.

Common Healthcare Mistakes Newcomers Should Avoid

Many healthcare problems happen because newcomers assume the Canadian system works the same in every province. A small misunderstanding can lead to delayed coverage or unexpected medical bills.

Avoiding these mistakes can protect both your health and your settlement budget.

| Mistake | Possible Risk | Better Approach |

|---|---|---|

| Assuming healthcare is free immediately | You may be uninsured during the waiting period. | Confirm your province’s start date before arrival. |

| Not buying private insurance | Emergency costs may be paid out of pocket. | Use private coverage until public coverage starts. |

| Ignoring dental and vision care | Unexpected expenses for checkups, glasses, or treatment. | Check student, employer, or private benefit plans. |

| Delaying health card application | Your access to insured care may be delayed. | Apply as soon as you meet eligibility requirements. |

| Not checking prescription coverage | Medication costs may become expensive. | Review drug benefits before choosing a plan. |

Final Thoughts

Healthcare in Canada is one of the strongest parts of the settlement system, but newcomers must understand that coverage is provincial, eligibility varies, and some services are not fully covered.

Permanent residents, work permit holders, and international students should check provincial rules, apply for health coverage early, and use private insurance if there is any gap. Prescription drugs, dental care, vision care, and emergency costs should also be part of your newcomer budget.

The safest strategy is simple: confirm your eligibility, protect yourself with insurance, and do not assume that every medical cost is covered automatically.