Recommended Blog Posts

- Spousal Sponsorship Canada 2026 – New Rules, Processing Time & How to Apply

- The Ultimate 2026 Guide: Canada PR for Software Developers (NOC 21232 / NOC 21231)

- What Are the Best Immigration Pathways for Nurses in Canada in 2026?

- Why a Good Credit Score Becomes Essential After Your ITA and Landing in Canada (Preparing for 2026)

- The Ultimate 2026 Guide: Canada Immigration From the UK

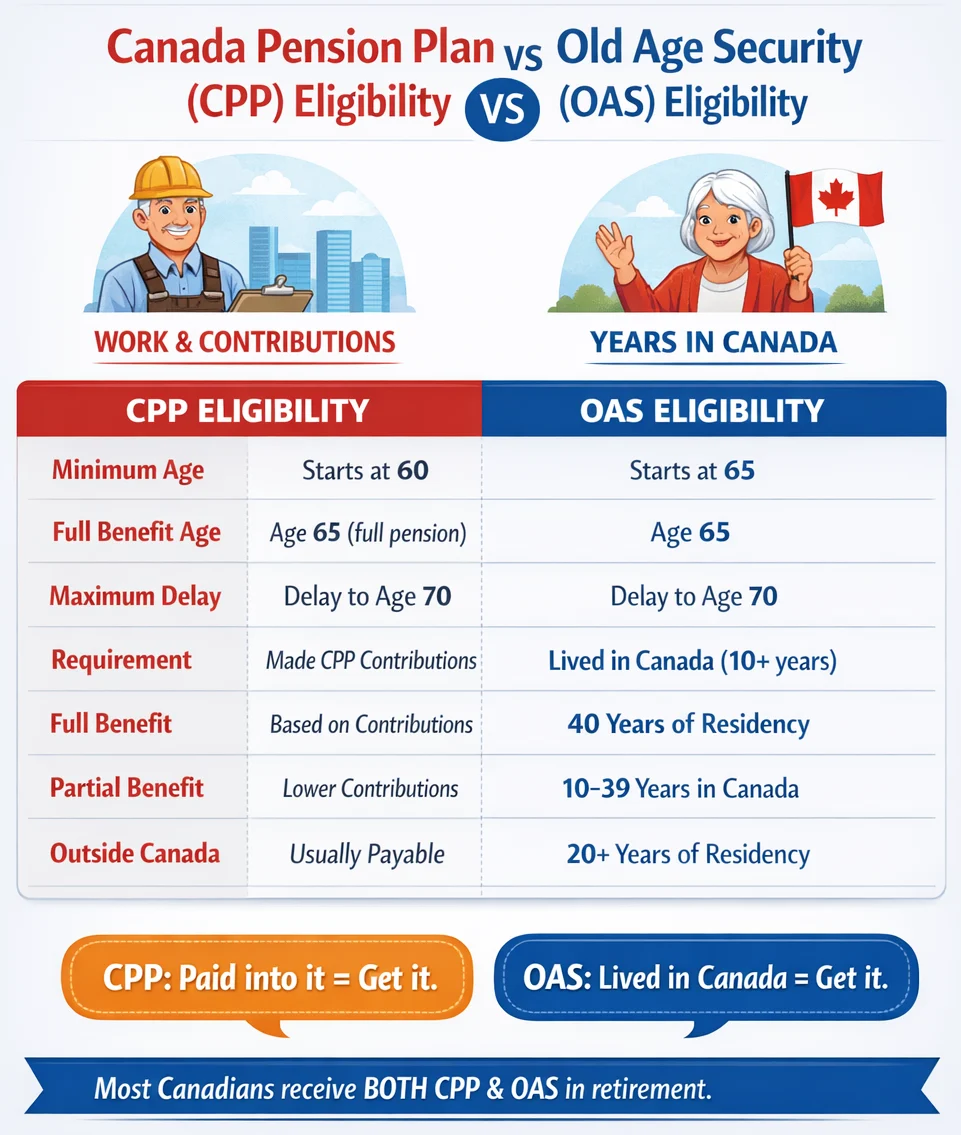

Eligibility for Canada Pension Plan (CPP) and Old Age Security (OAS)

Publish On: June 17, 2026

If you are planning retirement in Canada, two important public pensions you may hear about are the Canada Pension Plan (CPP) and Old Age Security (OAS). Many newcomers and permanent residents confuse the two, especially when it comes to residence rules.

The simplest way to understand the difference is this: CPP is based mainly on contributions from work in Canada, while OAS is based mainly on how long you have lived in Canada after the age of 18.

What Is the Difference Between CPP and OAS?

CPP and OAS are both public pension benefits in Canada, but they work differently.

CPP is a contribution-based pension. This means you may qualify if you worked in Canada and made valid CPP contributions through employment or self-employment.

OAS is a residence-based pension. This means your eligibility depends mainly on your age, legal status, and how many years you have lived in Canada after turning 18.

In simple terms, CPP depends on your contribution history. OAS depends on your residence history.

Canada OAS Eligibility: Who Can Receive Old Age Security?

To qualify for the Old Age Security pension, you must generally be 65 years of age or older.

If you are living in Canada, you must usually:

- Be a Canadian citizen or legal resident at the time your OAS application is approved.

- Have lived in Canada for at least 10 years since the age of 18.

If you are living outside Canada, you must usually:

- Have been a Canadian citizen or legal resident of Canada on the day before you left Canada.

- Have lived in Canada for at least 20 years since the age of 18.

This is why OAS is often important for immigrants and permanent residents who moved to Canada later in life. Your years of residence in Canada after age 18 directly affect whether you qualify and how much you may receive.

OAS Residency Requirements in Canada

The key OAS residency requirement is the number of years you lived in Canada after turning 18.

For most applicants:

| Situation | Minimum Residence Requirement |

|---|---|

| Living in Canada when applying | At least 10 years after age 18 |

| Living outside Canada when applying | At least 20 years after age 18 |

| Full OAS pension | Generally 40 years after age 18 |

If you have lived in Canada for less than 40 years after age 18, you may still qualify for a partial OAS pension. A partial OAS pension is generally calculated based on the number of years you lived in Canada divided by 40.

For example, if you lived in Canada for 20 years after age 18, you may receive 20/40ths, or 50%, of the full OAS pension amount, if you meet the other eligibility rules.

Can Immigrants Get OAS in Canada?

Yes, immigrants may be eligible for OAS if they meet the age, legal status, and residence requirements.

You do not need to have worked in Canada to qualify for OAS. This is one of the biggest differences between OAS and CPP.

A permanent resident who has lived in Canada for at least 10 years after age 18 may qualify for OAS while living in Canada, provided they meet the other eligibility conditions.

However, sponsored parents and grandparents should be careful. Some income-tested benefits, such as the Guaranteed Income Supplement, may be affected by sponsorship rules.

CPP Residency Requirements: Does CPP Depend on Residence in Canada?

This is where many people get confused. CPP does not work like OAS.

There is no standard “10-year residence rule” or “20-year residence rule” for CPP retirement pension eligibility. CPP is based on valid contributions, not residence years.

To qualify for a CPP retirement pension, you generally need to:

- Be at least 60 years old

- Have made at least one valid CPP contribution

Valid CPP contributions usually come from work you did in Canada. They may also come from pension credits received after a divorce or separation.

So, if someone searches for “CPP residency requirements,” the correct answer is that CPP does not have the same residence requirement as OAS. CPP depends mainly on whether you contributed to the plan.

CPP Eligibility Requirements in Canada

You may be eligible for CPP retirement pension if you are at least 60 years old and made at least one valid contribution to the Canada Pension Plan.

You can start CPP as early as age 60, but your monthly amount may be reduced if you start before age 65. You can also delay CPP after age 65, which may increase your monthly payment.

Your CPP amount depends on factors such as:

- How much you contributed

- How long you contributed

- Your average pensionable earnings

- The age you choose to start receiving CPP

- Whether you had low-income years, child-rearing periods, or other special situations

Unlike OAS, CPP is not automatically based on how long you lived in Canada.

CPP vs OAS Eligibility: Quick Comparison

| Feature | CPP | OAS |

|---|---|---|

| Full name | Canada Pension Plan | Old Age Security |

| Main basis | Work contributions | Residence in Canada |

| Minimum age | 60 | 65 |

| Need to work in Canada? | Yes, generally contribution-based | No |

| Need residence years? | Not in the same way as OAS | Yes |

| Available outside Canada? | Usually yes, if eligible | Yes, but residence rules apply |

| Full benefit depends on | Contribution history and earnings | Generally 40 years of residence after age 18 |

What If You Lived or Worked Outside Canada?

If you lived or worked in another country, you may still have options.

Canada has social security agreements with several countries. These agreements may help people qualify for CPP or OAS if they do not meet the standard requirements based only on their Canadian work or residence history.

For example, if you lived or worked in a country that has a social security agreement with Canada, time from that country may sometimes help you meet eligibility requirements. However, the payment amount may still depend on your actual Canadian residence or contribution history.

This is especially relevant for immigrants who moved to Canada later in life or Canadians who spent many years abroad.

Can You Receive Both CPP and OAS?

Yes, many people receive both CPP and OAS if they qualify for both.

You may receive CPP if you contributed to the Canada Pension Plan. You may receive OAS if you meet the age, legal status, and residence requirements.

CPP and OAS are separate benefits. Receiving one does not automatically mean you qualify for the other.

For example:

- A person who worked in Canada and contributed to CPP may qualify for CPP even with fewer years of residence.

- A person who never worked in Canada may still qualify for OAS if they meet the residence requirement.

- A newcomer who moved to Canada late in life may need to carefully check OAS residence rules before assuming eligibility.

When Should You Apply for CPP and OAS?

CPP can generally start as early as age 60, while OAS starts at age 65.

Some people may be automatically enrolled for OAS if Service Canada has enough information. If you are not automatically enrolled, you may need to apply.

Before applying, it is important to check:

- Your age

- Your years of residence in Canada

- Your CPP contribution history

- Whether you lived or worked in another country

- Whether a social security agreement may apply

- Whether your immigration or sponsorship history affects related benefits

Common Mistakes to Avoid

Many applicants make simple mistakes when checking CPP and OAS eligibility.

The most common mistakes include:

- Assuming CPP has the same residency rules as OAS

- Thinking OAS requires Canadian work experience

- Believing every permanent resident automatically qualifies for OAS

- Confusing OAS with GIS

- Not checking the 20-year rule before moving outside Canada

- Forgetting that partial OAS depends on years lived in Canada after age 18

- Ignoring social security agreements with other countries

- Understanding the difference between CPP and OAS can help you plan better and avoid delays.

Final Thoughts

Canada OAS eligibility and CPP requirements are different. OAS is mainly based on age, legal status, and residence in Canada. CPP is mainly based on work contributions.

For immigrants and permanent residents, the most important point is this: living in Canada matters for OAS, while contributing to CPP matters for CPP.

If you are unsure whether you qualify, review your residence history, contribution record, and immigration status before applying. For complex cases, especially where sponsorship, foreign work history, or time outside Canada is involved, professional Licensed RCIC guidance can help you avoid mistakes.